| DKK million | Note | 2017 | 2016 |

| Intangible assets | 3.1 | 2,432 | 2,737 |

| Property, plant and equipment | 3.2 | 8,926 | 8,641 |

| Investments in associates | 3.4 | 59 | 73 |

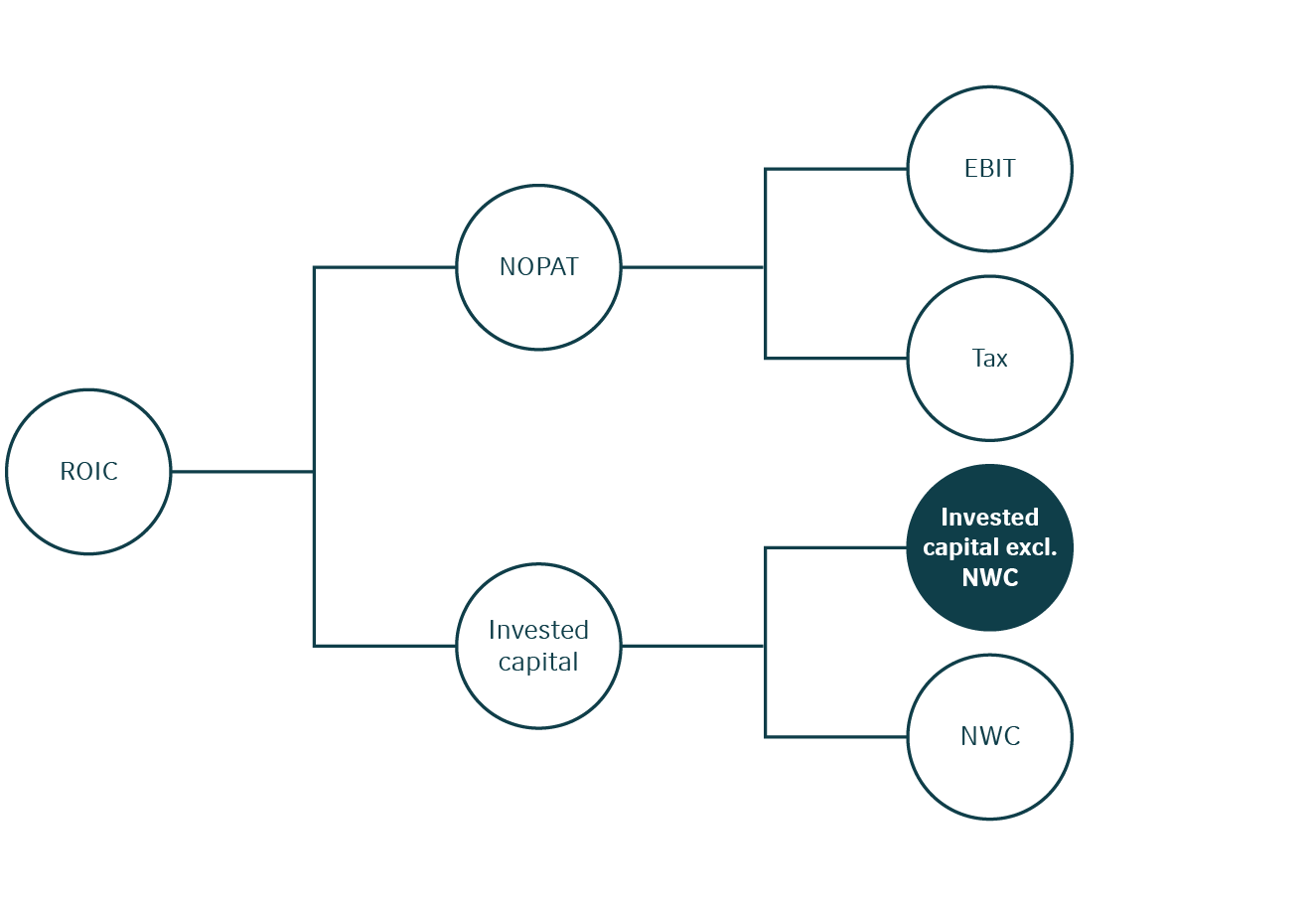

| Net working capital (see Net working capital section) | 2,023 | 2,088 | |

| Financial assets, non-interest-bearing | 16 | 4 | |

| Provisions | 3.3 | (245) | (292) |

| Other non-current financial liabilities, non-interest-bearing | (9) | (14) | |

| Other financial liabilities, non-interest-bearing | (8) | (111) | |

| Tax, net | (314) | (542) | |

| Invested capital | 12,880 | 12,584 | |

| Average invested capital | 12,732 | 12,238 | |

| DKK million | Goodwill | Acquired patents, trademarks, licenses and know-how, etc. | Completed IT development projects | IT development projects in progress | Total | |

| Cost at January 1, 2017 | 1,159 | 3,156 | 420 | 49 | 4,784 | |

| Currency translation adjustments | (51) | (35) | (1) | - | (87) | |

| Additions during the year | - | 7 | 10 | 82 | 99 | |

| Disposals during the year | - | (205) | (7) | - | (212) | |

| Transfers to/(from) other items | - | - | 70 | (70) | - | |

| Cost at December 31, 2017 | 1,108 | 2,923 | 492 | 61 | 4,584 | |

| Amortization and impairment losses at January 1, 2017 | (1,752) | (295) | (2,047) | |||

| Currency translation adjustments | 14 | 1 | 15 | |||

| Amortization during the year | (229) | (72) | (301) | |||

| Impairment losses | (27) | - | (27) | |||

| Disposals during the year | 201 | 7 | 208 | |||

| Amortization and impairment losses at December 31, 2017 | (1,793) | (359) | (2,152) | |||

| Carrying amount at December 31, 2017 | B/S |

1,108 | 1,130 | 133 | 61 | 2,432 |

Impairment

In 2017, an impairment loss of DKK 27 million on abandoned patents was recognized and included in Cost of goods sold and Research and development costs at DKK 15 million and DKK 12 million respectively.

Impairment test of goodwill

Since 2016, Management has identified two cash-generating units (CGUs): Novozymes’ main activities and the Albumedix Group. With the Albumedix divestment in late December 2017, the activity in the Albumedix CGU – now the Biopharma CGU – has been reduced to sales-based royalty agreements.

The market value of Novozymes is significantly greater than equity, thus no further key assumptions are used in determining whether impairment of goodwill exists for Novozymes’ main activities (2016: no impairment).

The recoverable amount of the Biopharma CGU has been determined based on a value-in-use calculation. The expected future cash flows are based on a forecasting period of four years, reflecting the term of the royalty agreements. The key assumptions used in testing for impairment are based on Management’s expectations of future royalty payments, which are partly based on experience, as well as input from external experts. Future royalty payments are on average expected to be on par with the realized royalty payments in 2017. A WACCWeighted average cost of capital. of 10% has been used to calculate the discounted cash flows for the Biopharma CGU.

As the value in use for the Biopharma CGU is greater than its carrying amount, no impairment has been identified (2016: no impairment)

| DKK million | Goodwill | Acquired patents, trademarks, licenses and know-how, etc. | Completed IT development projects | IT development projects in progress | Total | |

| Cost at January 1, 2016 | 1,140 | 2,912 | 349 | 24 | 4,425 | |

| Currency translation adjustments | (3) | 2 | 2 | - | 1 | |

| Additions from business acquisitions | 22 | 216 | - | - | 238 | |

| Additions during the year | - | 26 | 42 | 72 | 140 | |

| Disposals during the year | - | - | (20) | - | (20) | |

| Transfers to/(from) other items | - | - | 47 | (47) | - | |

| Cost at December 31, 2016 | 1,159 | 3,156 | 420 | 49 | 4,784 | |

| Amortization and impairment losses at January 1, 2016 | (1,487) | (262) | (1,749) | |||

| Currency translation adjustments | (1) | (2) | (3) | |||

| Amortization during the year | (224) | (51) | (275) | |||

| Impairment losses | (40) | - | (40) | |||

| Disposals during the year | - | 20 | 20 | |||

| Amortization and impairment losses at December 31, 2016 | (1,752) | (295) | (2,047) | |||

| Carrying amount at December 31, 2016 | B/S |

1,159 | 1,404 | 125 | 49 | 2,737 |

In 2016, an impairment loss of DKK 40 million on licenses was recognized and included in Cost of goods sold. The impairment loss was the result of an impairment test performed on a specific asset where indication of impairment had been identified due to reduced cash flow projections for the asset in question. The cash flow used for impairment was based on business plans for the period 2017-2021. A WACCWeighted average cost of capital. of 11% was used to calculate the discounted cash flows.

Management assesses the risk of impairment of the Group’s intangible assets. This requires judgment in relation to the identification of cash-generating units (CGUs) and the underlying assumptions in the Group’s impairment model.

If there is any indication of impairment, value in use is estimated and compared with the carrying amount. The calculation of value in use is based on the discounted cash flow method using estimates of future cash flows from the continuing use. The key parameters are the expected revenue streams and the rate used to discount the cash flows.

Intangible assets other than goodwill are measured at cost less accumulated amortization and impairment losses. Goodwill and IT development projects in progress are not subject to amortization.

Costs associated with large IT projects for the development of software for internal use are capitalized if they are incurred with a view to developing new and improved systems.

Amortization is based on the straight-line

method over the expected useful lives of the finite-lived assets, as follows:

Expected useful lives are reassessed regularly.

Research and development costs are expensed as incurred unless the criteria for capitalization are deemed to have been met. Due to significant uncertainty associated with the development of new products, research and development costs are not capitalized.

The Group regularly reviews the carrying amounts of its finite-lived intangible assets to determine whether there is an indication of an impairment loss. An impairment loss is recognized to the extent that the asset's carrying amount exceeds its estimated recoverable amount. Impairment losses are reversed only to the extent of changes in the assumptions and estimates underlying the impairment calculation.

Goodwill is tested for impairment annually or whenever there is an indication that the asset may be impaired.

| DKK million | Land and buildings |

Plant and machinery | Other equipment |

Assets under construction and prepayments | Total | |

| Cost at January 1, 2017 | 5,604 | 9,957 | 1,693 | 856 | 18,110 | |

| Currency translation adjustments | (291) | (527) | (88) | (37) | (943) | |

| Additions during the year | 65 | 294 | 110 | 1,124 | 1,593 | |

| Disposals during the year | (8) | (126) | (66) | (10) | (210) | |

| Transfers to/(from) other items | 45 | 210 | 30 | (285) | - | |

| Cost at December 31, 2017 | 5,415 | 9,808 | 1,679 | 1,648 | 18,550 | |

| Depreciation and impairment losses at January 1, 2017 | (2,673) | (5,718) | (1,078) | (9,469) | ||

| Currency translation adjustments | 116 | 268 | 29 | 413 | ||

| Depreciation for the year | (165) | (449) | (125) | (739) | ||

| Disposals during the year | 4 | 110 | 57 | 171 | ||

| Depreciation and impairment losses at December 31, 2017 | (2,718) | (5,789) | (1,117) | (9,624) | ||

| Carrying amount at December 31, 2017 | B/S |

2,697 | 4,019 | 562 | 1,648 | 8,926 |

| Of which assets held under finance leases | 59 | - | - | - | 59 | |

Capitalized interest and pledges

Interest of DKK 10 million (2016: DKK 4 million) has been capitalized under Additions during the year above and included as Investing activities in the statement of cash flows. Capitalization rate: 2.05% (2016: 1.78%).

Land and buildings with a carrying amount of DKK 377 million (2016: DKK 397 million) have been pledged as security to credit institutions. The mortgage loan expires in 2029.

Impairment

No impairment losses on property, plant and equipment have been recognized in 2017 (2016: no impairment losses).

| DKK million | Land and buildings |

Plant and machinery | Other equipment |

Assets under construction and prepayments | Total | |

| Cost at January 1, 2016 | 5,183 | 9,564 | 1,598 | 649 | 16,994 | |

| Currency translation adjustments | 31 | 42 | 11 | 11 | 95 | |

| Additions from business acquisitions | - | - | 2 | - | 2 | |

| Additions during the year | 326 | 197 | 82 | 530 | 1,135 | |

| Disposals during the year | (20) | (61) | (35) | - | (116) | |

| Transfers to/(from) other items | 84 | 215 | 35 | (334) | - | |

| Cost at December 31, 2016 | 5,604 | 9,957 | 1,693 | 856 | 18,110 | |

| Depreciation and impairment losses at January 1, 2016 | (2,518) | (5,327) | (987) | (8,832) | ||

| Currency translation adjustments | (11) | (9) | (5) | (25) | ||

| Depreciation for the year | (148) | (426) | (125) | (699) | ||

| Disposals during the year | 4 | 44 | 39 | 87 | ||

| Depreciation and impairment losses at December 31, 2016 | (2,673) | (5,718) | (1,078) | (9,469) | ||

| Carrying amount at December 31, 2016 | B/S |

2,931 | 4,239 | 615 | 856 | 8,641 |

| Of which assets held under finance leases | 59 | - | - | - | 59 | |

Property, plant and equipment is measured at cost less accumulated depreciation and impairment losses. Borrowing costs in respect of construction of major assets are capitalized.

Depreciation is based on the straight-line method over the expected useful lives of the assets, as follows:

The assets’ residual value and useful life are reviewed on an annual basis, and adjusted if necessary at each reporting date.

The Group regularly reviews the carrying amounts of its property, plant and equipment to determine whether there is any indication that those assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss, if any. If the recoverable amount of an asset is estimated to be lower than its carrying amount, the carrying amount is reduced to the recoverable amount. Impairment losses are reversed only to the extent of changes in the assumptions and estimates underlying the impairment calculation.

| 2017 | 2016 | ||||||

| DKK million | Dismantling and restoration | Legal, contingent consideration and other | Total | Dismantling and restoration | Legal, contingent consideration and other | Total | |

| Provisions at January 1 | 101 | 191 | 292 | 101 | 140 | 241 | |

| Currency translation adjustments | (7) | - | (7) | (1) | 1 | - | |

| Additions during the year | - | 21 | 21 | 1 | 72 | 73 | |

| Reversals during the year | (20) | (26) | (46) | - | (16) | (16) | |

| Utilization during the year | - | (15) | (15) | - | (6) | (6) | |

| Provisions at December 31 | 74 | 171 | 245 | 101 | 191 | 292 | |

| Recognized in the balance sheet as follows: | |||||||

| Non-current | B/S |

69 | 90 | 159 | 96 | 135 | 231 |

| Current | B/S |

5 | 81 | 86 | 5 | 56 | 61 |

| Provisions at December 31 | 74 | 171 | 245 | 101 | 191 | 292 | |

Dismantling and restoration

Dismantling and restoration relates to estimated future costs of environmental restoration – Novozymes aims for our production sites to have no negative environmental impact – and restoration of leased premises when terminating the lease and vacating the premises. These liabilities relate to established circumstances, and these costs are expected to be incurred either when concrete measures are implemented or when the sites are vacated. The expected costs and timing are by nature uncertain.

Amounts with regard to restoration of leased premises are considered uncertain, as the final settlements will depend on thorough inspection of the premises and negotiations with the lessor at the time of vacating. The costs are expected to be incurred in a minimum of 1 year to a maximum of 15 years.

Legal, contingent consideration and other

Novozymes is involved in a number of ongoing legal disputes, and provision is made for the estimated costs of these based on the current evaluation of the outcomes. The cases are expected to be finalized in 2018-2019. In Management's opinion, the outcome of these cases will not give rise to any significant loss beyond the amounts provided for at December 31, 2017.

Contingent consideration and other provisions cover a number of obligations, including liability for returned goods, contingent consideration, etc. Other long-term employee benefits are also included, but at only a minor amount, as the main part of Novozymes' pension plans are defined contribution plans, covering approximately 99% of employees. These obligations are mainly expected to be incurred over a long period.

Provisions are recognized where a legal or constructive obligation has been incurred as a result of past events and it is probable it will lead to an outflow of financial resources. Provisions are measured at the present value of the expected expenditure required to settle the obligation.

No provisions are discounted, as discounting does not have any significant impact on the carrying amounts.

Joint operations

In 2012, Novozymes formed a strategic partnership with Beta Renewables S.p.A. The parties have joint control of the partnership. The partnership had no material impact on revenueThe amount of money a company earns through the sale of goods and services. and earnings in 2017 (2016: no material impact), because biomassOrganic material, predominantly plants or plant residues. projects have not commercialized as expected in Beta Renewables. The contractual partnership expired in 2017, as renegotiations could not be completed due to financial difficulties in the M&G Group, the majority owner of Beta Renewables S.p.A.

Novozymes has interests in joint operations with Novo Nordisk. These are houseowners' associations and related utility facilities in connection with the shared Danish production sites in Kalundborg and Bagsværd. The operations had no impact on revenue and earnings in 2017 (2016: no impact). Novozymes and Novo Nordisk share control of the arrangements equally.

Associates

Novozymes holds 23.1% of the shares in Microbiogen Pty Ltd., with which Novozymes collaborates exclusively on the exploration and development of yeast for the ethanol industry.

Novozymes holds 19.35% of the shares in MagnaBioAnalytics LLC.

Novozymes holds 9.95% of the shares in Beta Renewables S.p.A., with which Novozymes formed a jointly controlled operation within biomass solutions up until 2017.

None of the associates is individually material to the Group.

| DKK million | 2017 | 2016 | |

| Associates | |||

| Share of result | I/S |

(14) | (31) |

| Comprehensive income for the year | (14) | (31) | |

| Investments in associates | B/S |

59 | 73 |

Joint operations

The Group’s holdings in joint operations are consolidated by including its interest in the joint operations' assets, liabilities, revenue and costs.

Associates

Investments in associates are accounted for using the equity method of accounting. Under the equity method, the investment in an associate is initially recognized at cost, and the carrying amount is increased or decreased to recognize Novozymes’ share of the profit or loss of the associate after the date of acquisition. The Group’s investment in associates includes the fair value of the net assets and goodwill identified on acquisition.

The accounting policies of associates have been changed where necessary to ensure consistency with the accounting policies adopted by the Group. Gains and losses resulting from transactions between the Group and its associates are recognized in the Group’s financial statements only to the extent of unrelated investors' investments in the associates.

In a step acquisition, the previously held equity interest in the acquiree is remeasured at its fair value on the acquisition date, and the resulting gain or loss is recognized in profit and loss. The estimated total fair value of the equity interest held immediately after the step acquisition is recognized as the cost of the equity interest.

No business acquisitions have taken place in 2017.

On September 15, 2016, Novozymes acquired 100% of the voting shares in Organobalance GmbH at a total purchase price of DKK 178 million. Organobalance GmbH owned a large collection of microbialRelating to or caused by microorganisms. strains and has strong capabilities in microbial screening and assay technology. The company is specialized in developing natural microbial solutions for customers and partners across a number of industries, including food, feed and animal health.

The purchase price allocation was finalized in 2016 and led to recognition of goodwill of DKK 22 million, intangible assets of DKK 216 million and a deferred tax liability of DKK 64 million.

The goodwill was attributable to expected synergies within Novozymes' existing microbial technologies and business areas. The goodwill was not tax deductible. The purchase agreement included a contingent consideration of up to DKK 30 million. In 2016, the cash outflow from the acquisition was DKK 146 million.

The consideration is contingent on achievement of a number of specific project development targets and sales targets in 2016-2018. DKK 12 million has been settled and the remaining part of the contingent consideration is unchanged.

On acquisition of companies, the identifiable assets acquired and the liabilities and contingent liabilities assumed are recognized at the fair values at the acquisition date. The consideration transferred includes the fair value at the acquisition date of any contingent consideration arrangement.

Goodwill may subsequently be adjusted for changes in the fair value of the consideration transferred and/or changes in the fair value of the identifiable net assets acquired until 12 months after the acquisition date, to the extent such changes relate to facts and circumstances present at the acquisition date. Acquired companies are consolidated from the date of acquisition. Acquisition-related costs are expensed as incurred.